Understanding Your Path to Affordable Recovery

Does insurance cover rehab? Yes, in most cases, health insurance does cover addiction treatment—often substantially. Thanks to federal laws like the Affordable Care Act (ACA) and the Mental Health Parity and Addiction Equity Act (MHPAEA), insurance companies are legally required to provide coverage for substance use disorder treatment as an essential health benefit, just like any other medical condition.

Quick Answer: What Insurance Typically Covers for Rehab

- Medical detoxification – Supervised withdrawal management

- Inpatient/residential treatment – 24/7 care in a facility

- Outpatient programs – Treatment while living at home (PHP, IOP, standard outpatient)

- Therapy sessions – Individual and group counseling

- Medication-assisted treatment (MAT) – Medications to support recovery

- Dual diagnosis treatment – Care for co-occurring mental health conditions

- Aftercare planning – Ongoing support and relapse prevention

If you’re struggling with addiction and worried about the cost of treatment, you’re not alone. In 2021, more than 46 million Americans suffered from a substance use disorder, yet 94% didn’t receive treatment. Cost is one of the biggest barriers keeping people from getting help.

The good news? Your insurance likely covers more than you think. Most health plans now include comprehensive addiction treatment benefits, and you may have little to no out-of-pocket costs depending on your specific plan.

This guide will walk you through exactly how to find out what your insurance covers, what types of treatment are included, and what to do if you don’t have insurance. We’ll help you understand your benefits so cost doesn’t stand between you and recovery.

, Step 2 - Know Coverage Types (Inpatient, Outpatient, Detox, Therapy, MAT), Step 3 - Verify Your Specific Plan (Call provider, check in-network status, understand costs), Step 4 - Explore All Payment Options (Medicare/Medicaid, payment plans, state programs, grants) - does insurance cover rehab infographic")

Your Right to Treatment: Laws That Mandate Rehab Coverage

Understanding your rights is the first crucial step in navigating insurance coverage for addiction treatment. You might be asking, does insurance cover rehab because it’s a medical necessity, or is it considered an elective service? Fortunately, federal legislation has clarified this, ensuring that addiction treatment is treated with the same importance as other medical conditions.

The landscape of health insurance coverage for substance use disorders (SUDs) has been significantly shaped by two landmark federal laws: the Affordable Care Act (ACA) and the Mental Health Parity and Addiction Equity Act (MHPAEA). These acts ensure that most health insurance plans must provide some level of coverage for addiction treatment.

How the ACA Impacts Insurance for Rehab

The Affordable Care Act (ACA), signed into law in 2010, revolutionized health insurance by making it more accessible and affordable for millions of Americans. A cornerstone of the ACA is its requirement for all new small group and individual insurance plans to cover a set of “Essential Health Benefits” (EHBs). Critically, mental health and substance use disorder services are included in these EHBs. This means that if your health insurance plan is ACA-compliant, it must provide coverage for addiction treatment.

One of the most impactful provisions of the ACA concerning addiction treatment is the elimination of denials based on pre-existing conditions. Before the ACA, insurance companies could refuse to cover individuals or charge them significantly more if they had a pre-existing condition, which often included addiction. Now, under the ACA, addiction is not considered a pre-existing condition that can be used to deny coverage or charge higher premiums. This ensures that a history of substance use does not prevent you from accessing the care you need.

The ACA treats addiction as a treatable medical disease, not a moral failing. This change in perspective has been instrumental in destigmatizing mental health and addiction within the U.S. healthcare system. For plans purchased through the Health Insurance Marketplace, addiction treatment is considered an essential health benefit that must be covered. This includes a broad range of services, from diagnosis and detoxification to various forms of therapy and ongoing support. We encourage you to explore the specifics of mental health and substance abuse coverage on Healthcare.gov.

Understanding the Mental Health Parity and Addiction Equity Act (MHPAEA)

Complementing the ACA, the Mental Health Parity and Addiction Equity Act (MHPAEA) of 2008 further strengthens your right to addiction treatment coverage. This law mandates that if your health plan offers mental health and substance use disorder benefits, it must do so at a level comparable to how it covers medical and surgical benefits. In simpler terms, your insurance cannot impose stricter limits on addiction treatment than it does on physical health treatment.

For example, MHPAEA prevents insurance companies from requiring more doctor visits, higher co-pays, or stricter authorization processes for addiction treatment compared to, say, treatment for a broken arm. If you are part of a group plan (such as what you’d receive from an employer) that includes more than 50 employees, the MHPAEA requires equal coverage. This means that cost-sharing, treatment limits, and care management requirements for mental health and substance use disorders must be no more restrictive than those for medical or surgical benefits.

The American Psychological Association highlights that when the ACA came into effect, it outlined that mental health conditions were to be treated with the same priority as physical health concerns. This principle, rooted in MHPAEA, means that substance use disorders are to be given the same level of coverage by insurance providers as physical health concerns. This parity law is a powerful tool in ensuring that financial barriers are reduced for those seeking help. You can learn more about the specifics of this act from the CMS.gov website.

What Types of Addiction Treatment Does Insurance Typically Cover?

Now that we understand the legal mandates, let’s dive into the specifics of what types of addiction treatment insurance typically covers. The answer to does insurance cover rehab often depends on the level of care deemed medically necessary and whether the treatment is evidence-based. Most insurance plans are designed to cover a comprehensive continuum of care, from initial medical interventions to long-term recovery support. At Pine Meadows Recovery, we offer a range of evidence-based treatments designed to support lasting recovery, which you can explore on our What We Treat page.

Does insurance cover inpatient vs. outpatient rehab differently?

Yes, insurance coverage can vary significantly between inpatient and outpatient rehab programs, primarily due to the intensity and cost associated with each.

-

Inpatient/Residential Treatment: This level of care involves 24/7 supervision and support within a facility. It’s typically recommended for individuals with severe substance use disorders, those requiring medical detoxification, or those who need a highly structured environment to achieve sobriety. Insurance generally covers inpatient treatment when it’s deemed medically necessary, meaning a doctor or clinical assessment determines it’s the most appropriate and effective level of care for your condition. However, authorization for inpatient care is often granted in short increments, sometimes just a few days at a time, requiring ongoing clinical updates to the insurer for continued coverage. Residential programs, while offering the highest level of care, are often the most expensive.

-

Outpatient Programs: These programs allow individuals to live at home while attending treatment sessions at a facility. They are generally less expensive than inpatient options and are suitable for those with stable living environments, strong support systems, or as a step-down from more intensive care.

- Partial Hospitalization Programs (PHP): Often referred to as day treatment, PHP involves attending therapy and counseling sessions for several hours a day, multiple days a week. We offer a comprehensive Partial Hospitalization (PHP) program.

- Intensive Outpatient Programs (IOP): IOPs offer a similar structure to PHP but with fewer hours per week, allowing for more flexibility. Learn more about our Intensive Outpatient Program.

- Standard Outpatient Programs: These are the least intensive, involving weekly or bi-weekly sessions. Our Outpatient Program provides flexible support for continued recovery.

Insurance companies assess the medical necessity for each level of care. If an individual can benefit from outpatient services, they may not authorize inpatient care. Coverage duration for any program can vary widely by policy, ranging from days or weeks to several months, depending on the plan’s specifics and ongoing clinical reviews.

Common Services Covered by Insurance

Most health insurance plans, particularly those adhering to ACA and MHPAEA guidelines, cover a wide array of evidence-based services essential for comprehensive addiction treatment:

- Medical Detoxification: This is often the first step in treatment, involving medically supervised withdrawal from substances. Insurance typically covers detox when it’s deemed medically necessary to manage potentially dangerous withdrawal symptoms.

- Individual Therapy: One-on-one counseling sessions with a licensed therapist are crucial for addressing underlying issues, developing coping mechanisms, and processing trauma. Common therapeutic models like Cognitive Behavioral Therapy (CBT) and Dialectical Behavior Therapy (DBT) are usually covered.

- Group Therapy: Participating in group sessions provides peer support, reduces feelings of isolation, and helps individuals practice communication and social skills in a safe environment.

- Dual Diagnosis Treatment: Many individuals struggling with addiction also have co-occurring mental health disorders, such as depression, anxiety, or PTSD. Comprehensive treatment that addresses both conditions simultaneously is typically covered, reflecting the understanding that these issues are interconnected.

- Medication-Assisted Treatment (MAT): MAT combines behavioral therapy and medications (like Suboxone or Methadone for opioid addiction) to treat substance use disorders and prevent relapse. Insurance often covers MAT, including the medications themselves, as it’s recognized as a highly effective, evidence-based approach.

- Aftercare Planning: This involves developing a relapse prevention plan, connecting individuals with sober support groups, and arranging ongoing therapy or counseling post-rehab. While not always a direct “service,” it’s integral to long-term recovery and often facilitated within covered treatment programs.

- Sober Living: While not always fully covered by all insurance plans, many plans will cover a portion of sober living or transitional housing, especially if it’s considered a clinically appropriate step-down from more intensive care, providing a supportive environment for individuals as they reintegrate into daily life.

While evidence-based treatments are generally covered, some holistic or alternative therapies might not be if they’re not deemed medically necessary or proven effective by the insurer’s standards.

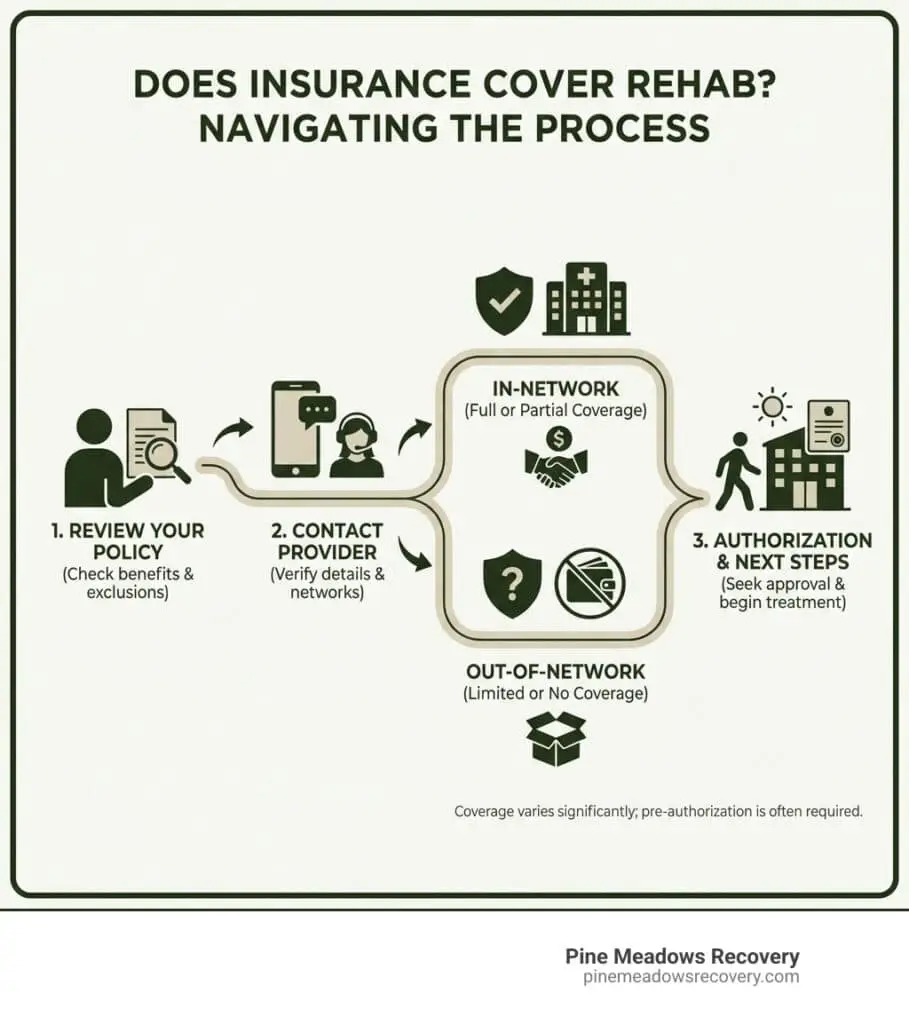

How to Verify Your Specific Insurance Plan’s Coverage

Understanding that federal laws mandate coverage is a great starting point, but the specific details of your plan are what truly matter. To answer the question, “does insurance cover rehab for me?,” you’ll need to verify your benefits directly. This process can seem daunting, but we’re here to guide you through it.

Understanding HMO vs. PPO Plans for Rehab

The type of health insurance plan you have will significantly impact how your rehab treatment is covered. The three most common types are Health Maintenance Organization (HMO), Preferred Provider Organization (PPO), and Point of Service (POS) plans.

| Feature | HMO (Health Maintenance Organization) | PPO (Preferred Provider Organization) | POS (Point of Service) |

|---|---|---|---|

| Network | Must use in-network providers, except for emergencies. | Can see both in-network and out-of-network providers, but with higher costs for out-of-network. | A mix of HMO and PPO. You choose a PCP within a network but can go out-of-network with a referral. |

| Referrals | Primary Care Physician (PCP) referral usually required to see a specialist. | No referrals needed to see specialists. | PCP referral is typically required to see specialists, especially for out-of-network care. |

| Cost | Generally lower premiums and out-of-pocket costs. | Higher premiums and deductibles, but more flexibility. | Costs can vary. In-network care is cheaper, while out-of-network care is more expensive. |

| Best For | Individuals who want lower costs and are comfortable with a limited network. | Individuals who want more choice and flexibility in choosing their healthcare providers. | A middle ground for those who want some flexibility but are willing to coordinate care through a PCP. |

How to ask “does insurance cover rehab?” effectively

- Call your provider: The most direct way is to call the member services number on the back of your insurance card.

- Use the insurance portal: Most insurance companies have online portals where you can check your benefits and find in-network providers.

- Speak with a treatment center’s admissions team: Reputable rehab centers, like Pine Meadows Recovery, have staff who can verify your insurance for you, often at no cost. This can save you time and confusion.

- Review your Summary of Benefits and Coverage (SBC): This document outlines what your plan covers and what you’ll pay for services.